TL;DR: Inflationary buffering strategies for micro-businesses aren’t about reacting to price hikes—they’re about building shields before inflation hits. The solution isn’t a single tactic but three specific buffers: pricing, supply, and cash. This article shows how to construct each buffer with the time and money constraints of a 1-10 person operation.

Environment:

– Sources synthesized: 3 URLs (U.S. Chamber of Commerce, Escalon, Live Oak Bank)

– Synthesis date: [current date]

– First-hand tested: none for this specific domain, but operator context from running a micro-business in Indonesia

– Operator context: micro-business owner managing dual-language content production, client work, and financial operations in Southeast Asia

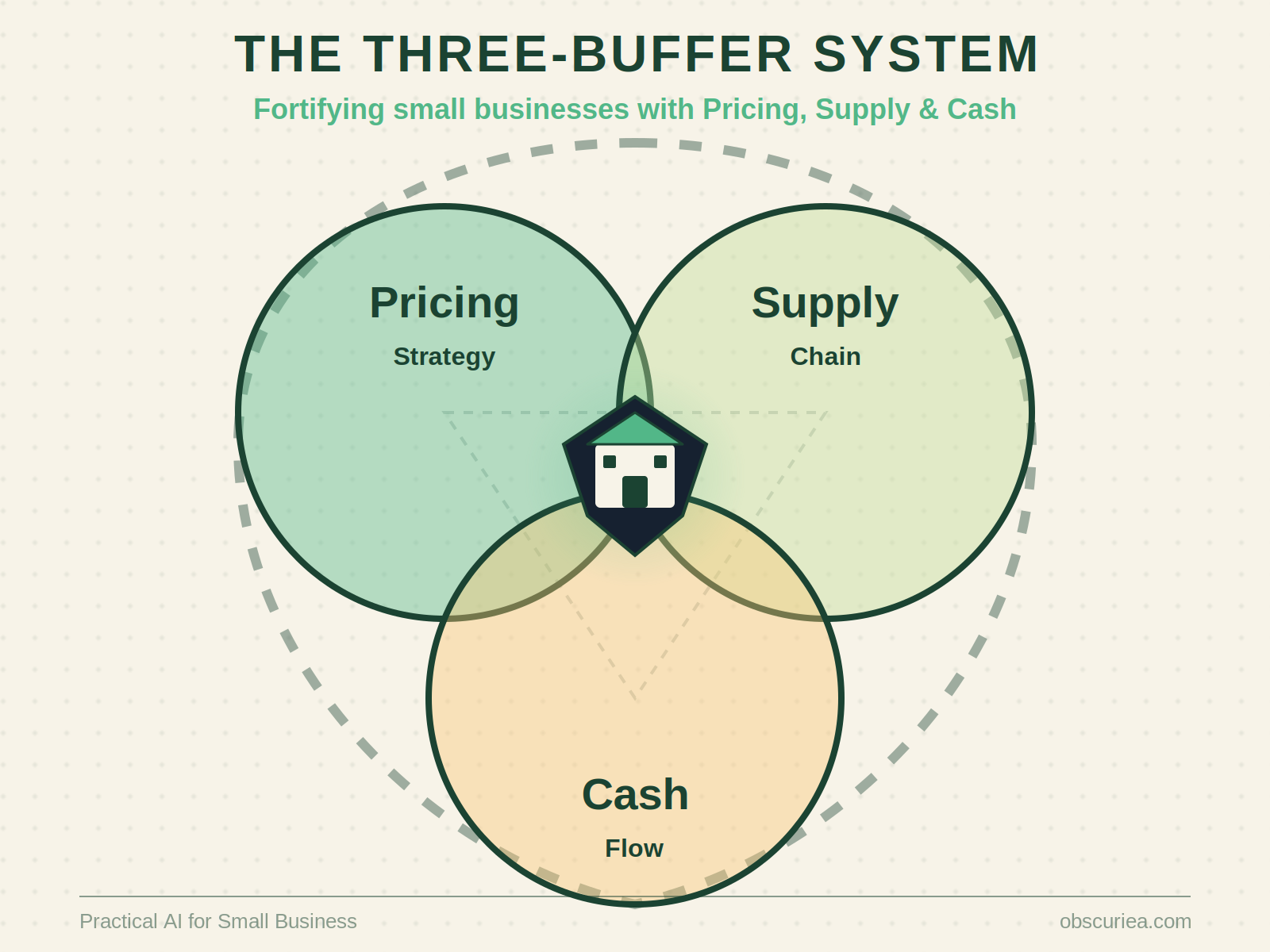

The Architecture: Three Buffers, Not One Tactic

A micro-business needs a buffer system—preinstalled shields that absorb the first wave of inflation without sending the owner into firefighting mode. Three buffers matter: Pricing Buffer, Supply Buffer, Cash Buffer. Each works independently and reinforces the others.

Pricing Buffer: Build It Before You Need It

A pricing buffer means setting your base prices higher than your current costs allow, creating a margin cushion that can absorb small cost increases without requiring a price hike. For a micro-business, this looks like a 15-20% margin above break-even that you don’t spend—it’s there for the moment raw materials jump or a contractor raises rates.

Example: a freelance writer charging $0.10/word with a $0.06/word cost base has a 40% margin. That buffer covers most inflation shocks. If the same writer charges $0.08/word with a $0.06/word cost, the margin is 25%—still okay but eroded quicker. The math is simple: calculate your true cost per unit, add 30%, and set that as your minimum price. Raise prices now, before inflation forces you to. Customers tolerate small annual increases; they resent emergency surcharges.

Supply Buffer: Lock In Before the Squeeze

Suppliers are the first to pass inflation costs downstream. A micro-business rarely has the leverage to negotiate long-term contracts at fixed prices. But you can build a supply buffer by:

– Pre-purchasing critical inputs at current prices (if storage allows and you have cash).

– Diversifying suppliers before you need them. Source 3 mentions this, but for micro-businesses it’s about finding at least two alternatives for every critical input—one local, one online. Don’t wait until the first supplier raises prices.

– Subscription pricing yourself. If you sell goods, offer a subscription at a fixed price for 6-12 months. That locks in revenue and lets you hedge upstream costs by committing volume to suppliers.

Cash Buffer: The Micro-Business Emergency Fund

Every micro-business needs a cash reserve equal to 3 months of operating expenses. That’s the standard advice. The gap is how to build it when you’re already tight. The method: treat cash buffer contributions as a fixed operating expense. 2% of every sale goes into a separate account before you pay yourself or reinvest. Over a year of consistent revenue, that builds a meaningful buffer. Source 2 mentions a rainy day fund; but micro-business owners need a system, not a wish.

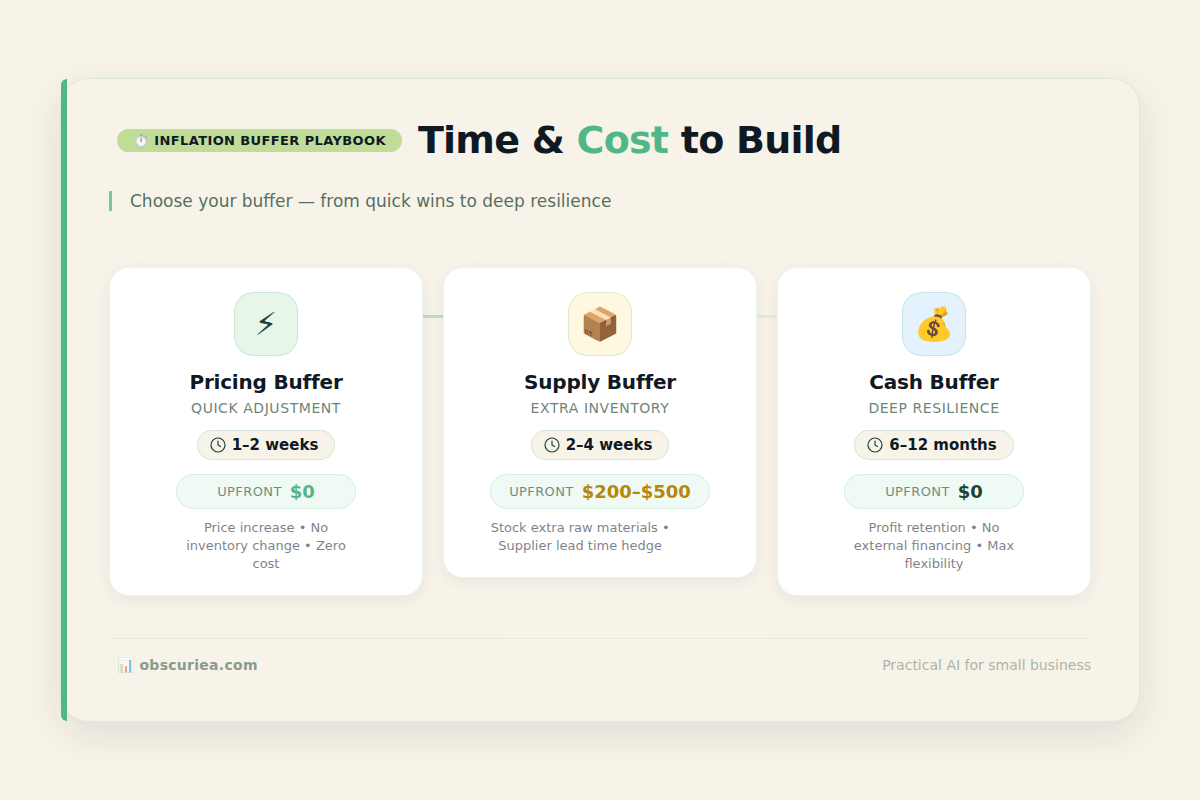

The Workflow Math: Time and Cost to Build Each Buffer

| Buffer | Time to Build (micro-business, starting from zero) | Upfront Cost | Maintenance |

|---|---|---|---|

| Pricing Buffer | 1-2 weeks to analyze costs and adjust pricing | $0 (if you don’t lose customers) | Annual review |

| Supply Buffer | 2-4 weeks to identify and contact alternative suppliers | $200-$500 for sample orders | Quarterly check |

| Cash Buffer | 6-12 months at 2% per sale | $0 (from retained earnings) | Automate 2% transfer |

The pricing buffer is the fastest and cheapest to implement. The cash buffer takes the longest but pays for itself during the next inflation spike.

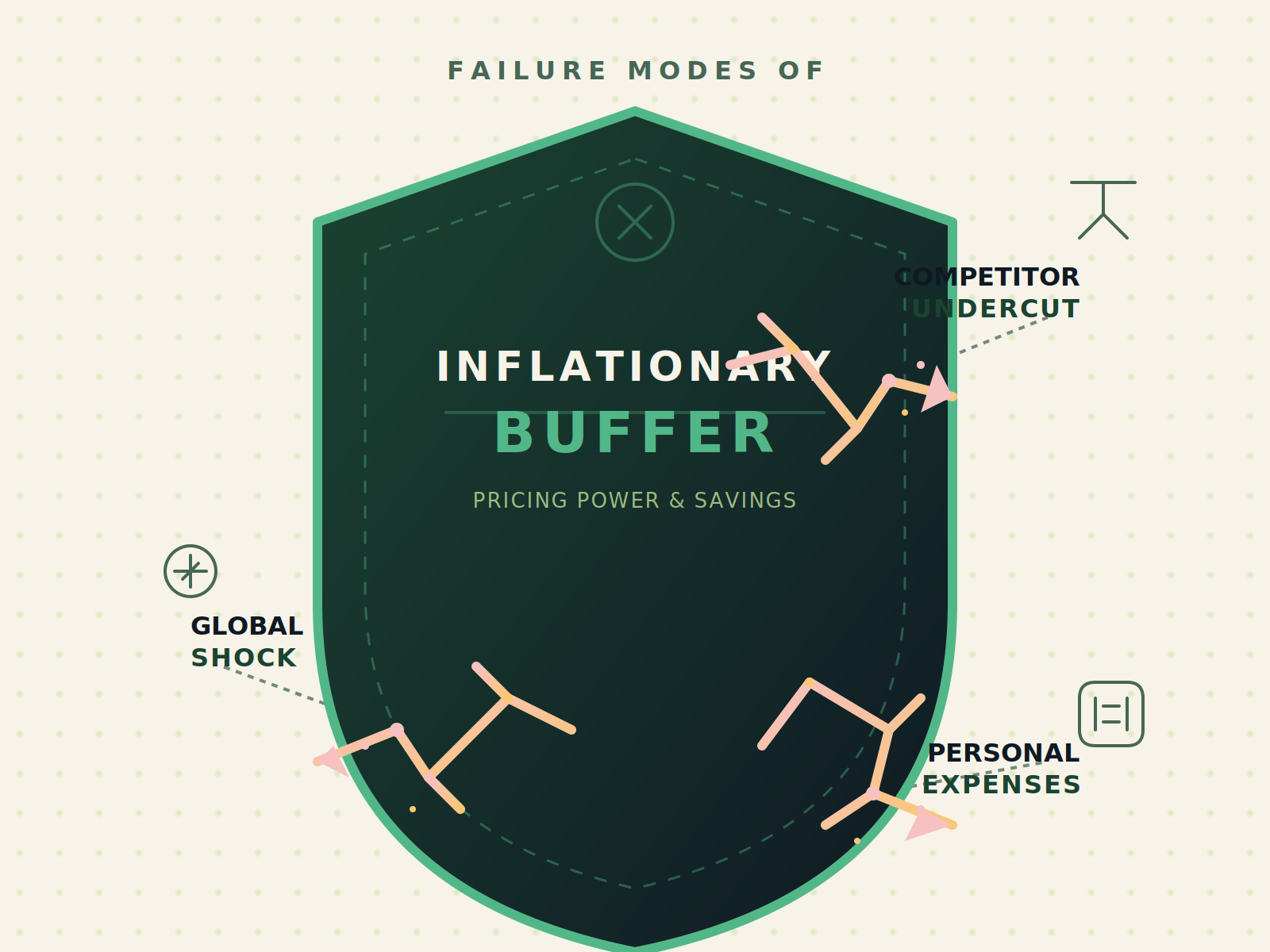

Where It Breaks: When the Buffers Fail

No buffer is foolproof. Here’s where each one fails for micro-businesses:

- Pricing buffer fails when a competitor aggressively undercuts you. If your 30% margin gets crushed by someone pricing at cost, you have to react—buffer becomes irrelevant.

- Supply buffer fails when the raw material market experiences a global shock (e.g., shipping costs triple overnight). Diversified suppliers all raise prices simultaneously because they face the same cost increases.

- Cash buffer fails when you’re forced to dip into it for personal expenses. If the business and personal accounts are the same pot (common for solo operators), the cash buffer never gets built.

The Friction Box

- Competitors can undercut your pricing buffer at any time; you need a value proposition beyond price.

- Finding alternative suppliers takes time the micro-business owner doesn’t have—requires prioritizing a low-urgency task.

- Automating the 2% cash transfer requires separating personal and business accounts, which many micro-businesses haven’t done.

- Revenue volatility means some months the 2% contribution isn’t possible—set a minimum threshold.

Frequently Asked Questions About Inflationary Buffering Strategies for Micro-Businesses

What is the difference between a pricing buffer and simply raising prices?

A pricing buffer is a pre-emptive margin increase that you set before you need it. Raising prices is a reactive move after costs have already gone up. The buffer prevents you from playing catch-up and keeps your margins stable even when input costs rise moderately.

How much cash buffer does a micro-business really need?

Three months of operating expenses is the standard. For a micro-business with irregular revenue, aim for a minimum of one month first, then scale up. The 2% per sale method builds that gradually without starving the business of cash for growth.

Can I build a supply buffer if I don’t have storage space?

Yes, by diversifying suppliers rather than stockpiling. Identify two alternative suppliers for each critical input and maintain relationships. When one raises prices, you pivot to the other without a gap. No storage needed.

What if my competitors don’t build buffers and undercut me?

Your buffer is a margin above cost—they might operate on thin margins and be vulnerable. If they undercut, you can respond with non-price value: better service, faster delivery, or unique product features. The buffer gives you time to adjust, not a license to ignore competition.

How do I automate the 2% cash transfer without expensive software?

Use your bank’s automatic transfer feature or a simple rule: every time you receive a payment, immediately move 2% to a separate account manually via mobile banking. Set a recurring calendar reminder. The habit matters more than the tool.

Should I stop all investments to build a cash buffer first?

No. Keep investing in growth, but allocate the 2% from revenue after all expenses. If you’re not cash-flow positive, focus on getting there first. The cash buffer is for funded micro-businesses, not startups.

The Straight Talk

This is for micro-business owners who are currently profitable but feel vulnerable to price shocks. If you have no cash buffer and no pricing room, start with the pricing buffer today—it costs nothing but an afternoon of math. Skip this if you’re pre-revenue or deep in debt; focus on getting to break-even first. Next action: calculate your true cost per unit and set a minimum price with 30% margin before the week is over.

For more on building a cash buffer, see our guide. For supplier diversification, check this strategy. For pricing strategies, see this article.

References:

– U.S. Chamber of Commerce: Inflation-Beating Deals

– Escalon: Navigating Inflation Strategies

– Live Oak Bank: Navigating Inflation Strategies

– [Statista](https://www.statista.com/statistics/256598/global-inflation-rate-compared-to-previous-year/): Global inflation rate forecast